刊于《加中金融》2020年8月

Published on Published on CCFA Journal of Finance, August 2020

200年前,一群荷兰人簇拥着大西洋上缓缓驶来巨轮,船上载着印度的香料、挪威的木材和中国的丝绸与瓷器,当然还有一大笔财宝,人们欢呼雀跃。

Two hundred years ago, a huge ship drifted slowly across the Atlantic Ocean. The vessel was manned by the Dutch, and filled with spices from India, timber from Norway, silk and ceramics from China, and, of course, no small amount of treasure. People celebrated their arrival.

海上的贸易充满了未知与凶险,每一次成功的返航都是劫后余生。船只是阿姆斯特丹造的,当初出海时大家都有出过一部分资金,一个叫阿德利安的人正在按比例分给人们贸易的利润。

Sea trade is always full of dangers and unknowns, meaning every successful return can rest on the role of a dice. Made in Amsterdam, the ship was collectively funded before the journey. Then, a man named Adrian distributed the trade profits in proportion.

这就是世界上第一个封闭式公募基金,人们给它取名“团结就是力量”。

This was the first closed-end publicly offered fund in the world, aptly named “Unity is Power”.

22年前,中国首批封闭基金发售,人们像炒新股一样摇号抢购,中国基金业萌芽破土。

Twenty-two years ago, China’s first closed-end funds were launched and snapped up like lottery tickets. This marked the beginning of the Chinese fund management industry.

中国基金业的生态与监管

The Chinese Fund Management Industry: Layout and Supervision

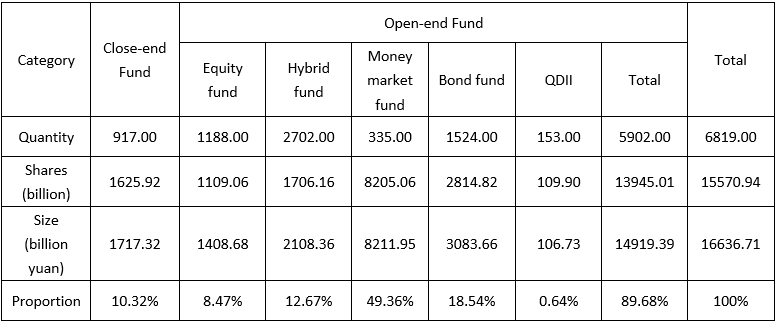

据基金业协会统计,截至2020年3月,全市场共有143家公募基金管理人,管理着6819只公募基金,规模合计16.64万亿元。2009年,全市场公募基金规模不到3万亿,也就是说,十年增长了5倍。

According to statistics from the Asset Management Association of China (AMAC), by March 2020, there were 143 publicly offered fund management companies on the market, managing 6,819 publicly offered funds with a total scale of RMB 16.64 trillion (USD 2.35 trillion). Comparing this with 2009, when there was less than RMB 3 trillion (USD 0.42 trillion) in publicly offered funds throughout the entire market, there has been a fivefold increase in just ten years.

具体到基金类型,其中货币基金占据半壁江山,其次是债券基金占比18.54%,股票与混合型基金合计分别占比8.47%、12.67%。

Narrowing this down to the specific types of funds, money market funds account for half of the amount, followed by bond funds at 18.54%, equity and hybrid funds 8.47% and 12.67% respectively.

过去四十年,中国经济高速发展,投资机会多,投资回报率高,资金无风险收益率居高不下。比如,信托产品收益率一度达到15%-17%,银行理财产品也有6%-8%的固定收益,久而久之就培养了居民的“刚兑习惯”。与之相对,作为新兴市场,国内资本市场波动很大,缺乏专业投资知识与长期投资理念的投资者很难赚钱,使得权益类基金产品的发展受到影响。2018年4月,《资管新规》落地,“产品净值化、破除刚兑”拉开序幕。同时,伴随无风险收益率不断走低,风险资产的性价比逐渐显现。

Over the past four decades, China has witnessed rapid economic development, numerous investment opportunities, high returns on investments, and consistently high risk-free returns on capital. For example, trust product return rates once reached 15%-17%, bank wealth management products (WMPs) generated stable return about 6%-8%. Over time, residents have developed a habit of “rigid redemption.” In contrast, as emerging market, the domestic capital markets are prone to acute fluctuations. As a result, investors who lack any professional investment knowledge and have no concept of how to invest in the long term often find it difficult to make any profit, which in turn hinders the development of equity funds. In April 2018, China’s New Asset Management Rules were implemented, and the “net-asset-value approachand rigid redemption break-down” policy was put in place. Meanwhile, as the risk-free return rate keeps falling, the cost effectiveness of risk assets has gradually become more apparent.

Source: Asset Management Association of China, as of 03/31/2020

Source: Asset Management Association of China, as of 03/31/2020

在中国资管行业中,基金行业的监管体系可能是最完备的。公募基金行业相关法规已经超过 210项,涵盖研究投资、交易风控、市场营销、清算运营、信息系统、法务合规等各个方面,强调信息公开透明、风险充分揭示、客户识别准确、流程完善清晰,成为银行资管、理财子公司、信托公司等资管机构转型过程中的参考典范。

The fund management industry is probably the most well-regulated sector in the Chinese asset management industry. There are more than 210 laws and regulations relating to the publicly offered fund management industry, covering areas such as research and investment, risk control, marketing, clearing operations, information systems, and legal compliance. These regulations exist in order to encourage open and transparent sharing of information, full risk disclosure, accurate customer recognition, and clear operational processes. The fund management industry has become the role model for other asset management institutions to aspire to during their transition, such as bank asset management firms, bank wealth management subsidiaries, and trust companies.

公募基金产品属于标准化的金融产品,制度领先,运作规范,是居民财富管理的重要配置工具,同时也在支持实体经济、资本市场改革中发挥着越来越重要的作用。为了进一步推动金融供给侧改革,推进金融服务实体经济,有效降杠杆、控风险,一方面,监管部门颁行《资管新规》,整肃资管行业内存在的刚性兑付、资金池业务、期限错配、通道业务等金融乱象,开启大资管行业净值化转型的新时代;另一方面,2019年10月,证监会优化公募基金产品注册机制,对诚信及合规风控水平较高、中长期投资业绩突出的基金管理人申报的常规产品实施快速注册,大力落实简政放权。同时,证监会加强事中事后监管,建立专项抽查复核工作小组,督促相关基金管理人确保申报材料的真实、准确、完整。

As a standardized financial product featuring leading systems and standardized operations, publicly offered funds have become an important wealth management tool for household asset allocation. Publicly offered funds play an increasingly crucial role in supporting the real economy and capital market reform. Two major changes have occurred as part of efforts to further push supply-side reform in the financial sector, promote real economy financial services, and effectively reduce leverage and control risks. Firstly, the China Securities Regulatory Commission (CSRC) enacted China’s New Asset Management Rules in order to rectify the chaotic practices that exist in the asset management industry, such as rigid redemption, cashpooling, and passageway business. This aimed to create a new era for net-asset-value products. Secondly, in October 2019, the CSRC optimized the registration procedures for public fund products. This provides speedy registration on conventional products for fund managers who have a high degree of integrity, sturdy compliance risk controls, and promising mid- to long-term investment performance. This came in an effort to streamline administration processes and decentralize power. At the same time, the CSRC has strengthened ongoing and follow-up supervision, and established a special task force to carry out spot checks and reviews, ensuring that the application materials provided by relevant fund managers are authentic, accurate and complete.

对于集中大量申报“同质化产品”,重募集轻管理,基金规模大进大出,不利于保护投资者利益等现象,监管也密切关注。2019年10月以来,权益产品的获批速度明显高于固收类产品,体现“扩大直接融资降杠杆”的政策导向。

The government also pays close attention to phenomena such as the large concentration of homogeneous products, an emphasis on raising capital instead of capital management, drastic changes of fund size , and actions that do not help protect the investor’s interests. Since October 2019, the policy orientation of “expanding direct financing and reducing leverage” has been reflected in the approval rate of equity products, which has been significantly higher than that of fixed income products.

新冠疫情的爆发,对基金行业的正常运作带来考验。一方面,员工人身安全与系统稳定性成为重中之重;另一方面,由于出行受限,出差调研和市场拓展等工作受到一定影响。此时,基金公司是否具有应急预案和灾备系统,是否具有细致的流程与严谨的执行力,是否具有积极进取和勇于拼搏的团队,就显得非常重要。同时,疫情也进一步彰显了数字化的重要性。例如,许多路演活动改为线上直播,许多调研活动也以电话会议、视频会议的形式展开。数字化是朱雀基金确立的三大战略之一,前期准备使我们较好地应对了新冠疫情的影响。

The outbreak of COVID-19 has challenged the normal operation of the fund management industry. In one respect, employer safety and system stability have become the top priorities; and additionally, due to travel restrictions, company visit research and market development have been affected to some extent. At this time, it is especially vital for fund management companies to have an emergency plan and disaster recovery system, meticulous processes and rigorous executive ability, and a bold, proactive team. The epidemic has also further highlighted the importance of digitization. For example, many roadshows have moved to online livestreaming, and a great number of research activities have been conducted in the form of teleconferences and video conferences. For Rosefinch Fund, digitization is one of the three established strategies that allows us to better cope with the impact of COVID-19.

美国基金业发展的启示

The Enlightenment of American Fund Management Industry Development

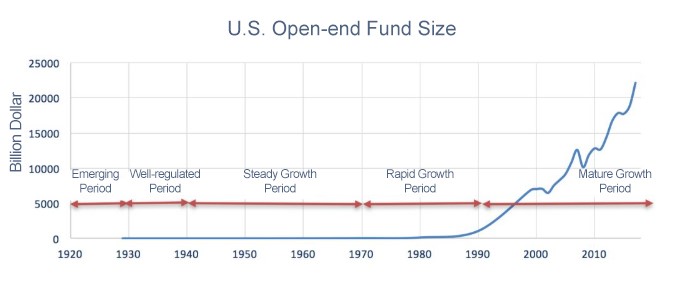

美国基金业已有百年历史,截至去年底,规模达25.7万亿美元,占据全球二分之一体量。根据发展节奏来划分,1970-1980年代是美国基金史上的分水岭。

The century-old US fund management industry reached a value of USD 25.7 trillion by the end of last year, accounting for half of the global total. Divided by their pace of development, the 1970s and 1980s were the watershed in the history of American funds.

Source: Huachuang Securities, ICI, 2018

如果说70年代是美国金融创新的开端,那么80年代就是蓬勃发展的高潮。共同基金规模从1970年的476亿美元上升到1980年的1347亿美元再到1990年的10652亿美元,数量上也从1970年的361只到1990年的3079只,一路高歌。结构上,货币型基金率先崛起,但80年代中后期股票型基金成为后起之秀。与此同时,免佣基金诞生,投顾模式兴起。

If the 1970s was the beginning of American financial innovation, the 1980s was its culmination. The AUM of mutual funds rose from USD47.6 billion in 1970, to USD 134.7 billion in 1980, then to USD 1.0652 trillion in 1990. The number of mutual funds rose from 361 in 1970 to 3,079 in 1990. Structurally, money market funds took the lead in this rise, but in the late 1980s, equity funds became the rising star. Meanwhile, the no-load fund was born and the Investor Advisory Service emerged.

这一时期,美元与黄金脱钩、金融监管放松、养老金入市、股权投资收益税收减免等等,都为共同基金的蓬勃发展提供了土壤。

During this period, the mutual funds were able to flourish based on changes such as the US dollar decoupling from gold, financial deregulation, the entry of pensions into the market, and tax breaks on equity gains.

此后,美国共同基金的发展形成了“税收优惠政策大力推动养老金入市-促进股权融资-企业盈利改善-经济向好-股指向上-养老金入市”的良性循环。尤其是个人养老金账户,为美国共同基金提供了长线资金,不仅推动了机构投资者的发展,也促使居民资产向证券市场转移。2020美国基金业年鉴显示,共同基金整体中,45%为股票型基金、21%为混合型基金、11.8%为债券型基金、货币基金占比仅为6.9%。45.5%的家庭持有共同基金,相比1980年的5.7%增加了十倍。

Since then, the development of mutual funds in the United States formed a positive cycle, starting with the creation of tax preferential policies to promote the market entry of pensions. This then promotes equity financing, improves corporate earnings, strengthens the economy, increases the stock index, and successfully achieves pension market entry. Individual pension accounts, in particular, provide long-term funding for US mutual funds, promoting not only the development of institutional investors, but also the transfer of household assets to the securities market. According to Investment Company Fact Book 2020, 45% of existing mutual funds are equity funds, 21% are hybrid funds, 11.8% are bond funds and only 6.9% are money market funds. 45.5% of households hold mutual funds, a tenfold increase from 5.7% in 1980.

在中国,公募基金仅占居民资产的3.5%,其中货币基金占比六成,权益基金不到三成,远远低于美国的水平。

In China, publicly offered funds only account for 3.5% of household assets, with money market funds accounting for 60% and equity funds less than 30%, far below the levels seen in the US.

但可喜的是,与80年代的美国类似,中国近年来也在推进一系列资本市场改革:构建和完善养老三支柱,推动养老金、企业年金入市;推出科创板、新三板精选层,开启科创板、创业板注册制,不断完善资本市场基础性制度;加大资本市场对外开放,取消外资持股比例限制;推进金融供给侧改革,大力发展直接融资……参照上世纪80年代美国公募基金行业的快速发展,我们相信中国的公募基金行业在前期22年的发展基础之上,将迎来更大的发展机遇。

However, there is also cause for optimism. Similarly to the US in the 1980s, over the past few years China has been advancing a series of capital market reforms. We have constructed and improved the three pillars of pensions to promote the use of pension and enterprise annuities to enter the market. In order to continuously improve the basic capital market system, we have launched STAR Market and the New Third Board selection floor, as well as implementing the new registration system for the STAR Market and the Gem Board. We have further opened up the capital market to foreign investment and removed foreign shareholding limits. We have promoted financial supply-side reform and intensively developed direct financing. Using the rapid development of the US publicly offered fund management industry in the 1980s as our point of reference, we believe that the Chinese publicly offered fund management industry can expect to see greater opportunities for development, based on the previous 22 years of development.

中外合资基金公司的现状

Current Status of Chinese-Foreign Joint Venture Fund Management Companies

在143家持有公募牌照的机构中,中外合资企业有43家,占比近三分之一。截至2019年12月31日,中外合资基金公司管理的资产规模合计达7万亿元人民币,占全行业近一半。2019年,据Wind不完全统计,20家有营收数据的中外合资基金公司营业收入均为正;26家有净利润数据的中外合资基金公司中的25家净利润为正。具体分布如下图:

Of the 143 institutions in China with publicly offered fund licenses, 43 are joint ventures, accounting for nearly a third. As of December 31, 2019, the assets managed by Chinese-foreign joint venture fund companies totaled RMB 7 trillion, which is half of the industry. In 2019, according to incomplete statistics provided by Wind, the operating incomes of the 20 Chinese-foreign joint ventures (with revenue data) were all positive. Of the 26 Chinese-foreign joint ventures (with net profit data), 25 had positive net profit. The specific distribution is as follows.

统计显示,中外合资公司的盈利水平呈梯队式分布,差异较大。净利润排名前十的机构中,中外合资公司占3席,分别为工银瑞信基金(15.36亿元)、建信基金(12.38亿元)、华夏基金(12亿元)。观察第一梯队的公司,其共性在于本土化程度较高。本土化意味着与中国市场的结合更为紧密:投资端,能结合A股上市公司的特性进行研究,挖掘价值;资金端,能够体察不同类型投资者的诉求,提供贴切的产品方案。

Statistics show that the profit of Chinese-foreign joint ventures are distributed in a clear hierarchy, with great differences between each level. Among the top 10 institutions, there are three Chinese-foreign joint ventures, namely ICBC Credit Suisse Asset Management (RMB 1.536 billion), CCB Principal Asset Management (RMB 1.238 billion), and China Asset Management (RMB 1.2 billion). If we observe this top level of high-profit companies, we can see that what they share is a high degree of localization, meaning closer integration with the Chinese market. In terms of investment, this means that research into the combined features of A-share listed companies can help to discover value. With regard to capital, we can observe the demands from different types of investors and provide the appropriate product solutions for them.

以1990年交易所开市为起点,今年A股迎来而立之年。尽管与海外市场相比还很年轻,但中国的资本市场不乏自身特色。对于计划进入中国的海外资产管理人而言,我们认为最重要的是“When in Rome, do as the Romans do. ”(入乡随俗)无论是合资还是独资企业,充分了解中国市场的特点,包括资本市场制度、法律环境、资金属性、资产特征等方方面面,才能更好地发展。

If 1990 marks the birth of the Chinese stock exchange, this year, A-share companies have now reached its thirties. Although still a newcomer in comparison with overseas markets, China’s capital markets have their own unique characteristics. For overseas asset managers planning to enter China, we believe the key thing to remember is “When in Rome, do as the Romans do”. Whether they are a joint venture or a wholly-owned enterprise, they should do their utmost to properly understand the Chinese market, including the capital market system, legal environment, capital attributes, asset characteristics and so on. Only by fully understanding these features will foreign investors be able to achieve substantial development.

当然,随着金融开放陆续推进,外资在A股的话语权将逐步增强。当前A股流通市值28.7万亿,除去大股东、产业资本等长线资金,实际在市场上活跃的流通市值可能就在15万亿附近,若外资以每年几千上万亿的速度流入,将成为关键的边际增量资金。

Of course, in the gradual process of opening up financially, the influence of foreign capital over A-shares will gradually increase. At present, the current market value of A-shares is RMB 28.7 trillion. Excluding long-term funds such as major shareholders and industrial capital, the actual free floated market value is around RMB 15 trillion. If foreign capital flows in at a rate of one trillion yuan per year, it will become the key marginal incremental capital on the market.

基金投顾改革

Fund Investment Advisory Reform

今年4月,证监会发布《证券基金投资咨询业务管理办法(征求意见稿)》,目前仍在征求意见阶段。

In April this year, the CSRC published the Administrative Measures on Securities Funds Investment Advisory Business (Draft for Comment), which is currently soliciting opinions from the public.

基金投顾改革的主旨在于,在销售层面,要站在客户的角度,做买方投顾而非卖方销售。卖方销售的重心在于服务卖方(基金公司),为基金产品做分销,并从中获得佣金;而买方投顾的重点在于为买方(基金投资者)提供配置建议,收取顾问费用。

The purpose of the fund investment advisory reformis located at the sales level, wherein we should share the same perspective as the buyer, acting as their investment consultant rather than a sales representative for the seller. The main focus of a sales approach is to serve the seller (fund companies) by distributing their fund products and receiving commission in return. Conversely, the focus of investment consulting is to provide the buyer (fund investors) with advice on how to allocate their assets, charging them consultancy fees for this service.

相较传统模式,买方投顾机制有利于引导居民合理配置基金产品,避免“基金赚钱,基民亏钱”的现象屡屡发生,一方面提升投资者的“获得感”,另一方面使得基金管理人免受短期波动的干扰,专心投资做好长期业绩,以便形成良性循环。那些业绩优秀、风格稳定、特征鲜明的主动管理人将获得更多青睐。

Compared with the traditional method, investment consulting mechanisms help buyers distribute their capital into the most reasonable fund products available, working to avoid the situation where the fund makes money, but the investors are losing money. On one side, we should be improving investors’ sense of fulfillment from investing. On the other side, we should be safeguarding fund managers against interference from short-term fluctuations, and focusing on making investments that perform well in the long term. By succeeding on both of these fronts, we can form a self-sustaining cycle. The active managers who prove themselves to have outstanding performance, a consistent investment style and distinctive characteristics will be more widely favored by both investors and fund companies.

但是,基金投顾改革需要时间去培育,不会一蹴而就。据统计,中国仅约6%的基民在购买基金前会接受专业投顾的指导,而在美国,这一比率大约是50%。这其中,专业投资顾问的培养是一个方面,投资者对专业服务付费意识的培养是另一个方面。

However, there is still a long way to go in reforming fund investment advisory system, it is certainly not going to happen overnight. Statistics indicate that only about 6% of Chinese fund investors will receive professional guidance before purchasing funds, while in the United States, this figure stands at nearly 50%. This can be attributed to two reasons: the training of professional investment consultants, and the investors’ awareness of how paying for professional services can benefit their investments.

推进基金投顾业务,除了培养专业化人才,利用科技手段也非常重要。最近几年,智能投顾在海内外都迅速发展。去年6月,蚂蚁金服与Vanguard集团合资成立先锋领航投顾,二者分别持股51%和49%。今年4月,二者合作的基金投顾服务“帮你投”在支付宝上线,目前已获得35万的财富号关注人数。

In addition to training professional consultants, it is vital that we take advantage of technology as a way of promoting the fund investment consulting business. In recent years, intelligent investment consulting has developed rapidly both in China and abroad. In June last year, Ant Financial Services Group and Vanguard Group jointly set up Xianfeng Linghang Tougu (Shanghai) Investment Consultancy Company, 49% of which is owned by Vanguard and 51% by Ant Financial. In April this year, the “Help You Invest” service was launched by Alipay, and has already attracted 350,000 followers.

与国内现存的投顾服务相比,“帮你投”依托先锋集团的专业投资能力与蚂蚁金服强大的互联网基因,特点是“快诊断”“低费率”及“低门槛”。打开小程序,系统即可一键诊断出用户的风险偏好,比如“动态进攻”,对应年化9%的投资目标。然后,匹配策略组合,股票型基金70%,债券型基金28%,货币型基金2%。据了解,诊断的依据是用户在支付宝上的消费行为和理财习惯。投资门槛只有800元,远远低于国外的高门槛服务。投顾费用按年化总资产的0.5%收取,体现了普惠金融的定位。

Compared with the existing investment advisory services in China, “Help You Invest” relies on Vanguard Group’s professional investment capabilities and Ant Financial’s strong background in Internet services to form such features as “fast judgement,” “low rate” and “low threshold” investments. When users open the mini program, with one click the system can make a judgement for on their “risk appetite,” such as “dynamic attack,” corresponding to an annualized investment objective of 9%. Then, the program matches fund portfolios, 70% for equity funds, 28% for bond funds and 2% for money market funds. According to our understanding, the judgement is based on user’s consumption behavior and financial habits on Alipay. The minimum required investment is RMB 800, far lower than the high threshold for such services in foreign countries. The user will be charged a 0.5% annual fee on assets under management, which reflects the move towards inclusive financing.

但是,对于首次接触蚂蚁金服的投资者,或进行多平台理财的投资者而言,一分钟诊断的准确性有待商榷。此外,组合中的股票型基金仅仅涵盖指数基金(且以宽基指数为主,暂未涉及行业主题指数),与近几年中国资本市场结构化的投资机会之间存在匹配不足的问题。

However, the accuracy of the one-minute judgement is questionable for investors who are new to Ant Financial, or for investors who manage assets across multiple platforms. In addition, the equity funds in the portfolio only cover index funds (mainly broad-based indexes; sector-based indexes are not yet supported), which is not sufficiently matched with the structured investment opportunities of China’s capital market in recent years.

据蚂蚁金服数字金融总裁黄浩介绍,他们在支付宝上发起了一个关于客户喜欢怎样理财方式的小调查。目前,该调查已有8万多人参与,结果显示84%的人觉得理财要靠自己,只有16%选择找人打理。可见,基金投顾服务的发展还任重道远。

Huang Hao, president of digital finance at Ant Financial, introduced that the company launched a small survey on Alipay about customers’ financial management methods. So far, more than 80,000 people have participated in the survey. 84% of recipients said they wanted to manage their money on their own, and only 16% said they were looking for someone to manage their money for them. Clearly, there is still a long way to go for the development of fund investment consulting services.

金融市场对外开放

Opening up Financial market

“走出去”与“引进来”是金融开放的两扇门。

“Bringing in” and “going global” are the two pathways for opening up the financial market.

为了给投资者提供多元化的资产配置,境内投资机构可通过 QDII或港股通“走出去”,投资境外资产。目前,158家境内机构具备QDII资格,额度总计1039亿美元。其中,44家公募基金公司有361亿美元的QDII额度,截至6月,共存续296只QDII基金,规模261亿美元。不过,囿于对海外市场的理解程度,不少QDII基金的主要配置方向是海外中概股。

In order to provide investors with more diversified asset allocation, domestic Chinese investment institutions can “go global” through QDIIs (Qualified Domestic Institutional Investors) or Hong Kong’s Stock Connect to invest in overseas assets. At present, 158 domestic institutions are qualified for QDII, at a total figure of USD 103.9 billion. Among them, there are 44 publicly offered fund companies with a QDII quota of USD 36.1 billion. As of this June, there are still 296 QDII funds remaining, with a total of USD 26.1 billion. However, many QDII funds are mainly allocated to overseas China concept stocks, owing to limited understanding of overseas markets.

过去十年,外资在A股的话语权不断提升,与政策支持“引进来”密不可分。海外投资者持有A股市值的比率,从2010年的0.3%上升至2020Q1的3.1%,是增长最快的一类投资者。外资的流入主要通过两个渠道:QFII/RQFII和陆港通(包括沪港通与深港通)。截至2020Q1,两者的总规模达到1.7万亿元,日益成为中国资本市场中一支不可忽视的力量。

Over the past ten years, foreign capital has held an increasing sway in A-shares, which is closely linked to the policy support designed to bring in foreign investment. The proportion of overseas investors holding A-shares rose from 0.3% in 2010 to 3.1% in 2020 (Q1), making this the fastest growing category of investors. The inflow of foreign capital is mainly passing through two channels: QFII/RQFII (RMB Qualified Foreign Institutional Investor) and the Stock Connect (including the Shanghai-Hong Kong Stock Connect and the Shenzhen-Hong Kong Stock Connect). By 2020 (Q1), the total scale of these two channels has reached RMB 1.7 trillion, and they are constantly proving themselves as a force to be reckoned with in the Chinese capital market.

2019年7月,国务院金融稳定发展委员会办公室公布了11条金融业进一步对外开放的政策措施,并宣布将原定于2021年取消证券公司、基金管理公司和期货公司外资股比限制的时点提前到2020年。今年4月1日起,中国允许国外机构设立全资子公司。

In July 2019, the Financial Stability and Development Committee under the State Council released 11 measures to further open up the financial sector to foreign participation, and announced that the deadline for removing foreign shareholding restrictions in the securities, fund management and futures sectors has been brought forward by a year to 2020. Since April 1 of this year, foreign institutions have been allowed to set up wholly foreign-owned subsidiaries in China.

2019 年 9 月 10 日,外管局宣布全面取消合格境外投资者(QFII)和人民币合格境外机构投资者(RQFII)的投资额度限制。2020年5月7日,相关政策进一步细化和落地,金融开放步伐向前,境外投资者参与境内金融市场的便利性大幅提升,外资流入将是长期趋势。作为A股市场重要的增量资金,外资的边际影响逐渐增强,将促进A股走向成熟的机构化市场。

On September 10, 2019, SAFE (State Administration of Foreign Exchange) announced that it would completely abolish restrictions on the investment quotas for QFII and RQFII. On May 7, 2020, the related policies will be refined further and fully implemented. With the pace at which financial opening up moving forward, the convenience for overseas investors to participate in Chinese financial markets will be greatly improved, meaning that there will be a substantial long-term inflow of foreign capital. As an important incremental capital in the A-share market, the marginal influence of foreign capital is gradually increasing, helping to turn the A-share market into a mature, institutional market.

“外来的和尚”是否会对本土选手形成威胁呢?海外机构的核心竞争力主要体现在完善的制度流程、体系化的投研规范、严谨的风控框架和国际化视野,尤其在衍生品定价和交易能力上更具优势。而国内公募基金管理人可能更熟悉国内的经济环境、法规体系、市场特征和投资者行为,在股票、债券等基础资产的投资管理方面更具优势。

Will this foreign competition pose a threat to our local players? The core competencies of overseas institutions mainly consist of sound institutional processes, systematic investment and research standards, rigorous risk control frameworks and an international mindset, especially in the pricing of derivatives and trading capabilities. However, domestic public fund managers may be more familiar with the domestic economic environment, the regulation systems in place, local market characteristics and Chinese investor behavior. Furthermore, Chinese publicly offered fund managers have more advantages in managing underlying assets such as stocks and bonds.

其实,中国的基金行业一直在加强开放。目前,中外合资基金公司占总数的1/3以上。基金业起源于西方,中国作为后来者不断学习借鉴,在22年的发展历程中也诞生出一批体量大、实力强、品牌好、业绩优、产品广、渠道多的基金公司。

Indeed, China’s fund management industry has been greatly increasing its degree of openness. At present, Chinese-foreign joint venture fund companies account for more than one third of the total fund companies. The fund management industry originated from the West, and China, as a latecomer, has gone great lengths to study and learn from the industry. After the industry’s 22 years of development in China, a group of fund companies have emerged that are large in size, highly capable, well branded, produce excellent results, have a wide range of products and diverse channels at their disposal.

无论姓“中”还是姓“外”,基金管理人的宗旨都是“给持有人创造价值”。我们认为,构建资管公司核心竞争力有五个关键点:

Whether a fund manager is “Chinese” or “foreign,” their aim always lies in “creating value for the holders.” As far as we are concerned, there are five key points in building the core competencies of asset management companies:

1)投研能力,这是资管公司持续成长的核心问题。

2)战略选择,即公司如何定位?是定位指数型基金,还是主动管理基金?是定位权益基金,还是固收基金?

3)以人力资源管理为代表的管理能力。

4)产品设计能力,国内同时还应注重市场营销能力。

5)品牌力。品牌需要长时间的积累,而非一劳永逸。

1) Investment and research capability, which is the core issue in ensuring the continuous growth of asset management companies.

2) Strategic choices, as in, how does the company position itself? Index investment or active investment? Equity investment or fixed income investment?

3) Management ability, which can be represented by human resources management.

4) Product design capability. In China, marketing is also important.

5) Brand influence. Brands need to be built to last for a long time, not to be a one-fix solution.

结合朱雀团队十余年的发展历程,我们谈谈感悟:

Looking back over more than a decade of the Rosefinch team’s development, here are some of our thoughts:

1)投研能力上,朱雀基金聚焦产业链研究,在能力范围之内,力争在某个领域,成为核心公司的主要股东。我们要站在行业的最高点去思考行业的变革,思考行业未来可能出现的变化和风险。与其把握短线机会,我们更注重企业未来的5~10年的发展。

1) In terms of investment and research capabilities, the Rosefinch Fund focuses on industrial chain research and strives to, within its capabilities, become a major shareholder of a core company in a certain field. We should situate ourselves at the highest point of an industry in order to properly think about how it may be transformed, and the potential changes and risks in the future. Instead of taking short-term opportunities, we pay more attention to a company’s development over the next 5-10 years.

2)战略选择上,我们选择了从私募转向公募。10多年前私募基金大发展,朱雀团队创业的时候,整个私募基金行业的AUM是200多亿,2015年发展到十几万亿,私募管理人也从几十家发展到两万家,势必加大了监管的难度。在这样的情况下,我们选择做公募,更严格的监管意味着更强的信任背书,同时也能享有政策红利。

2) Our strategic choice has been to shift from private fund to public fund. More than 10 years ago, private fund industry underwent rapid development. When the Rosefinch team started business, the total AUM (Asset Under Management) of private fund industry was over RMB 20 billion, reaching more than RMB 10 trillion in 2015. Private fund managers also increased from just dozens to 20,000, which inevitably made supervision incredibly difficult. It was in this context that we applied for public fund license. Stricter supervision means stronger trust endorsement; meanwhile, we could enjoy policy dividends.

3)团队管理上,我们不强调“王重阳”,而是着力培养自己的“七子剑阵”。我们做了两件事情,一件是重塑合伙制,通过员工持股打造优秀团队;另一件是数字化建设,我们的产业链研究与数字化升级就有很大关系。

3) As for team management, we are not looking to train erudite talents like Wang Chongyang (one of the founders of the Quanzhen School of Daoism), but focus on training our own elite team, like the Seven Masters of Quanzhen (Wang Chongyang’s legendary disciples). In view of this, we have done two things. One is to reshape our partnership mechanism, creating exceptional teams by granting shares to key members. The other is digital construction, as our industrial chain research is closely related to digital upgrading.

4)负债端建设上,负债端与资产端的长期匹配一定要做到,要努力让自己的“口袋比较深”,且资金结构良好。朱雀基金目前的管理规模中,机构客户占比超过了60%,机构客户中的产业客户占比超过60%,换句话说,我们有40%的资金来自于产业资本。这使我们可以更好地践行产业链研究、长线投资的理念。

4) With regard to reinforcing the liability side of the balance sheet, we have made it imperative to achieve long-term matching between liabilities and assets. We should strive to deepen our pockets, so to speak, and create a sound capital structure. In the Rosefinch Fund’s current management scale, institutional clients account for more than 60%, within which industrial clients constitute more than 60%. In other words, 40% of our funds come from industrial capital. This enables us to better practice industrial chain research and long-term investment.

随着中国经济的转型升级和资本市场基础性制度建设的不断完善,中国资产管理行业发展前景巨大。而包括海外投资者在内的专业机构投资者的发展加剧了行业的竞争。朱雀基金将坚持权益类资产的主动管理这一核心战略,不断打造自身能力圈,聚焦先进制造、TMT、大消费、医药生物等产业链,以实现为投资人持续创造价值的愿景,力争成为海外华人和机构投资者分享中国企业持续成长、走向世界的平台。

With the transformation and upgrading of China’s economy and the continuous improvement of the basic systems in the capital market, China’s asset management industry has massive prospects for development. The development of professional institutional investors, including overseas investors, has intensified competition in the industry. Rosefinch Fund will adhere to active management of equity assets as our core strategy, continuously building our capability circle and focusing on industrial chains such as Advanced Manufacturing, TMT (Technology, Media, Telecom), Big Consumption, Healthcare. Together, this is designed to achieve our vision of constantly creating value for investors. We are striving to become a platform for overseas Chinese and institutional investors to share the continuous growth of Chinese enterprises and go global, together.

参考资料:

华宝证券《2020年中国金融产品年度报告:财富管理新时代》

中信证券《A股投资者结构全景扫描》

Investment Company Fact Book 2020

申万宏源证券《溯源美国基金业:养老体系完善、市场机构化、股指长牛、被动投资、兴盛的四方循环》

References

1. HWABAO Securities. 2020 China Financial Product Annual Report: A new era of wealth management.

2. CITIC Securities. Overview of A-share investors structure.

3. Investment Company Fact Book 2020.

4. Shenwan Hongyuan Securities. Trace to the American fund management industry:the four-aspect cycle of perfect pension system, institutionalized market, long term bull market indicated by the stock market index , passive investment and prosperity.

版权所属:家族办公室 - Family Office Times,如若转载,请注明出处:https://www.fott.top/archives/12836/

微信扫一扫

微信扫一扫